-

-

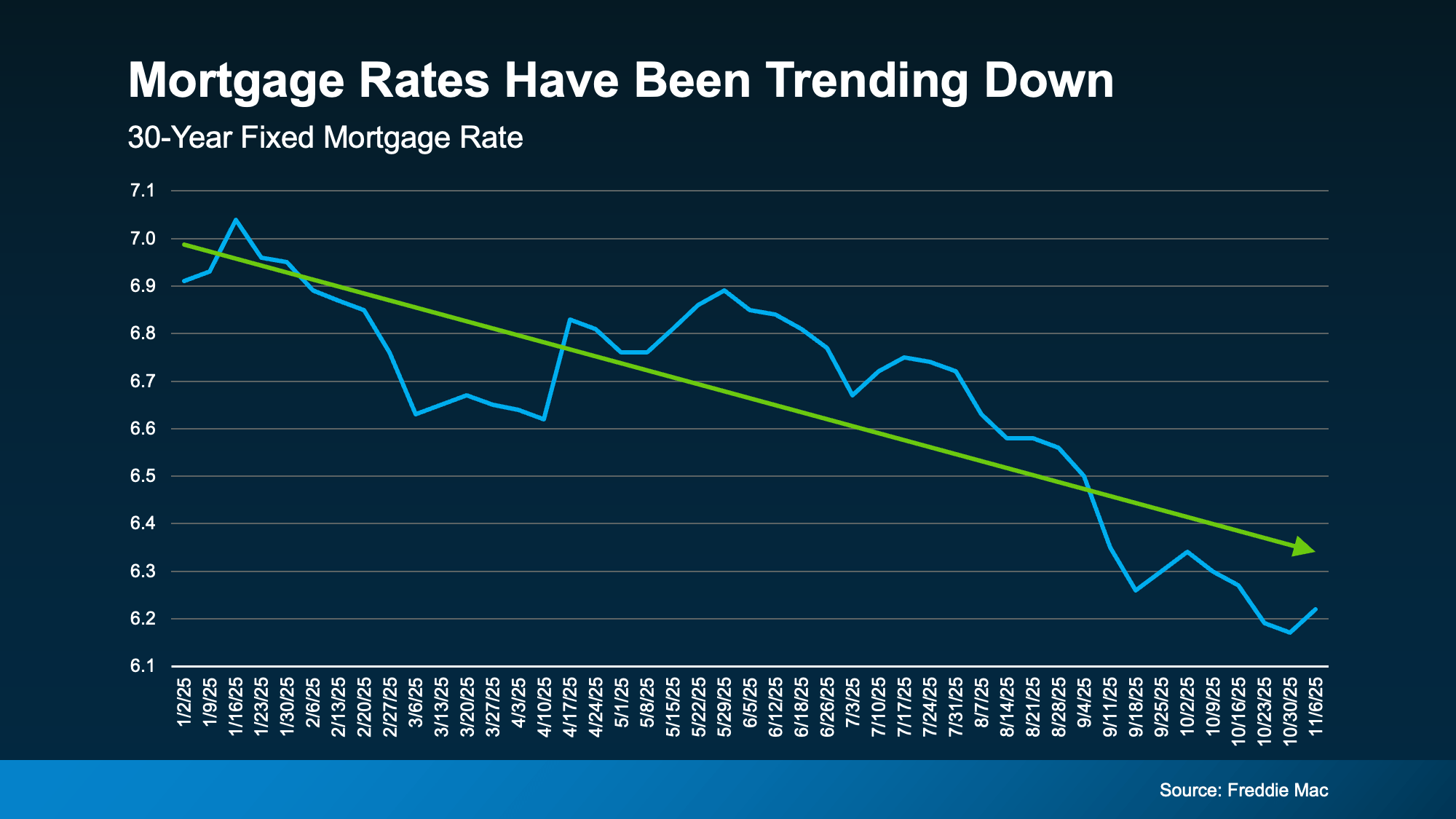

Mortgage rates have recently dipped into the high 5% range but are mostly hovering in the low 6s. In this week’s market insight, we look at what that actually means for buyers and why waiting for the “perfect” rate may not make as much difference as many people think—especially as we head into the spring market here in Upland and throughout the Inland Empire....

Read more

-

-

In today’s market, many parents and grandparents in Upland and throughout the Inland Empire are wondering how they can help the next generation achieve the dream of homeownership. If you’ve built substantial equity over the years, you may have more opportunity than you realize. This week’s newsletter explores how your home’s equity could become a meaningful way to create stability, security, and legacy for someone you love — without compromising your own future....

Read more

-

-

The Upland and Inland Empire housing market is showing real momentum as we close out the year. Inventory is up, rates are easing, and buyers and sellers finally have more breathing room. Here’s what these trends mean for you....

Read more

-

-

A quick look at how falling rates, rising inventory, and renewed buyer activity are quietly shifting the housing market heading into 2026....

Read more

-

-

The Fed meets Sept. 17 to decide on interest rates, with markets leaning toward a cut. While inflation is still above target, a softer job market has shifted the Fed’s focus. Mortgage rates have already dipped to their lowest point in nearly a year, offering some relief — but high prices and limited inventory continue to challenge buyers....

Read more

-

-

With job growth slowing and unemployment ticking up, many are wondering if the Federal Reserve will cut rates at their September meeting. A softer labor market could mean lower mortgage rates ahead—creating opportunities for buyers, sellers, and homeowners alike....

Read more

-

-

August 2025 housing market update: home prices, sales, and trends. Learn what rising inventory and steady values mean for buyers and sellers.

August real estate update: discover housing market trends, home values, and selling insights for homeowners in today’s shifting market.

Housing market report August 2025: prices, inventory, and sales data. Get insights on whether now is the right time to buy or sell.

August housing market update: see the latest trends in home values, sales, and in...

Read more

-

-

August 2025 housing market update: home prices, sales, and trends. Learn what rising inventory and steady values mean for buyers and sellers.

August real estate update: discover housing market trends, home values, and selling insights for homeowners in today’s shifting market.

Housing market report August 2025: prices, inventory, and sales data. Get insights on whether now is the right time to buy or sell.

August housing market update: see the latest trends in home values, sales, and in...

Read more

-

-

Discover what’s driving today’s real estate market in Upland and the Inland Empire, from shifting inventory to local price trends, and what it means for your next move....

Read more

-

-

Expert tips for first-time homebuyers from Upland Realtor Sonja Coffee. Learn how to get pre-approved, set a budget, and buy your first home with confidence....

Read more

-

-

Is Now a Good Time To Sell? You Bet.

Despite the headlines, buyers are still active—especially here in the Inland Empire. Roughly 84 homes are selling daily in our area. Life isn’t slowing down, and neither is the real estate market. If you’re thinking of selling, let’s create a smart strategy and get your home sold.

...

Read more

-

-

The market is shifting—but that’s not bad news. Learn what today’s changes mean for sellers and how to make smart moves in a more balanced housing market....

Read more

-

-

Is Your Home Still the Right Fit?

Life changes fast—and sometimes, our homes can’t keep up. This week, I’m sharing why more homeowners are choosing to move despite higher rates, and how real-life needs like space, family, and health are outweighing the numbers. If you’ve been feeling stuck, this might be the perspective you need....

Read more

-

-

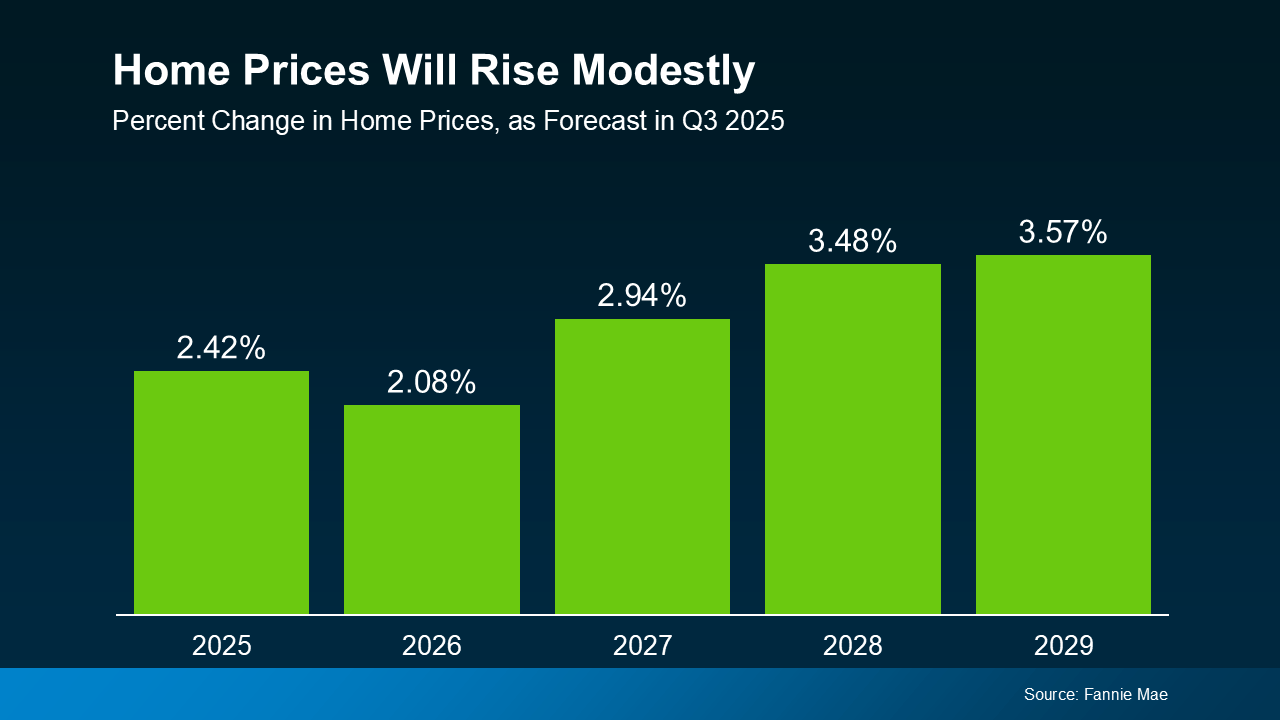

Thinking of waiting to buy a home? You could end up paying more. Experts predict home prices will continue to rise steadily through 2029. In this update, learn why acting sooner, even if it’s not the perfect moment, I can help you build wealth over time.

...

Read more

-

-

Spring is bringing fresh energy to the Inland Empire housing market.

With more inventory hitting the market and mortgage rates stabilizing, buyers have more options—and sellers have more opportunity. Plus, the best week to list your home this year is just around the corner: April 13–19. If you’re thinking about selling, now is the time to get your home ready and take advantage of the seasonal momentum....

Read more

-

-

Need help understanding your current policy or securing the best coverage for your needs? Call Dori Ferranto with Ferranto Fields Insurance Services for expert guidance on policies and renewals....

Read more

-

-

Disaster Relief Resources: Shelter, Food Assistance & Wildfire Recovery...

Read more

-

-

The housing market is always shifting, and 2025 will be no different. With rates likely to ease a bit and prices rising at a more normal and sustainable pace, it’s all about staying informed and making a plan that works for you....

Read more

-

-

Online home valuations often rely on limited data and miss key factors like a home’s condition, local trends, and real-time comparable sales. As a seasoned real estate expert with over two decades of experience, I can provide a more accurate assessment and ensure you set the right price for your property. Let’s work together to reveal your home’s true value....

Read more

-

-

Political uncertainty, economic shifts, and Federal Reserve policies are causing mortgage rates to fluctuate, making it crucial to rely on expert guidance for informed real estate decisions....

Read more

-

-

Even if you’re not looking to move right away, you may have questions about how the election will impact the housing market. When we look at historical trends, combined with what’s happening right now, we can find your answers. Based on historical data, mortgage rates decrease in the months before and home prices and sales increase the year after the election. The facts show Presidential elections only have a small and temporary impact on the housing market....

Read more

-

-

What To Expect from Mortgage Rates and Home Prices in 2025

With mortgage rates expected to ease and home prices projected to rise at a more moderate pace, 2025 is shaping up to be a more promising year for both buyers and sellers.

If you have any questions about how these trends might impact your plans, let’s connect. That way you’ve got someone to help you navigate the market and make the most of the opportunities ahead....

Read more

-

-

Thinking about moving in 2025? Here’s what experts say you can expect. Mortgage rates are projected to come down. More homes are expected to sell. And prices are forecast to go up. Let's connect to talk about what this means for your plans to move....

Read more

-

-

Myths About the 2024 Housing Market...

Read more

-

-

Unlock the secrets to selling your home successfully in Southern California's competitive real estate market with our expert tips. Learn how to highlight your property's best features, attract motivated buyers, and achieve top dollar for your home. From enhancing curb appeal to strategic pricing and effective marketing, my proven strategies will help your listing stand out in the crowded landscape. Partner with me to maximize your home's potential and navigate the selling process w/c...

Read more

-

-

As we celebrate International Women's Day, let us reaffirm our commitment to advancing women's equality and empowerment. Let us recognize the achievements of women past and present, while also acknowledging the work that lies ahead. Together, we can create a world where every woman and girl can realize her full potential, free from discrimination and inequality....

Read more

-

-

As we celebrate International Women's Day, let us reaffirm our commitment to advancing women's equality and empowerment. Let us recognize the achievements of women past and present, while also acknowledging the work that lies ahead. Together, we can create a world where every woman and girl can realize her full potential, free from discrimination and inequality....

Read more

-

-

Merry Christmas, and Thank you. ...

Read more

-

-

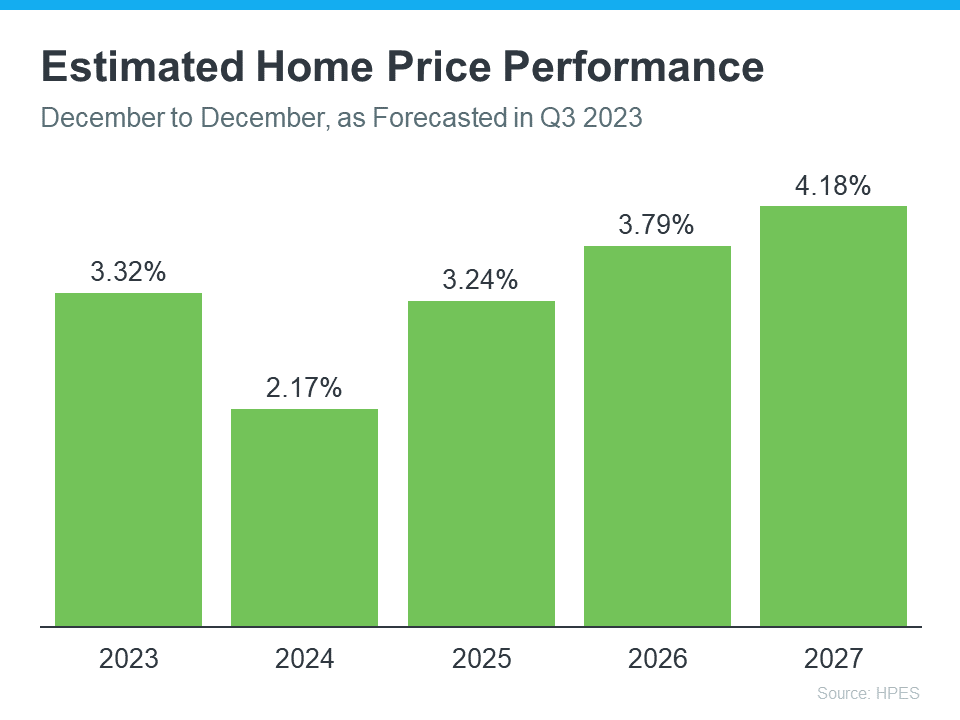

If you’re someone who’s worried home prices are going to fall, rest assured a lot of experts say it’s just the opposite – nationally, home prices will continue to climb not just next year, but for years to come...

Read more

-

-

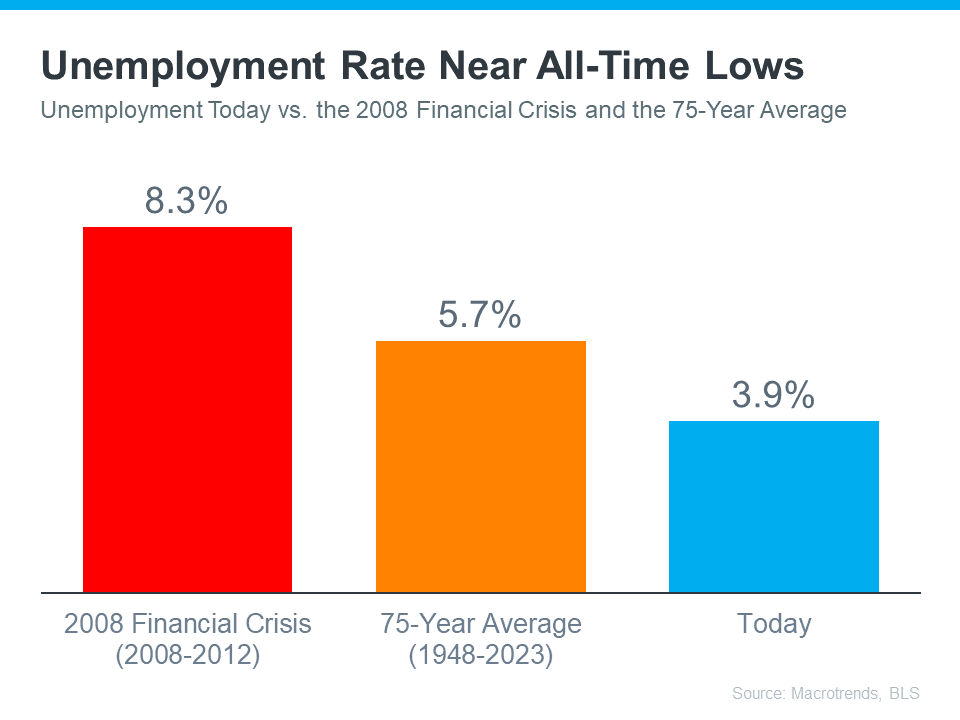

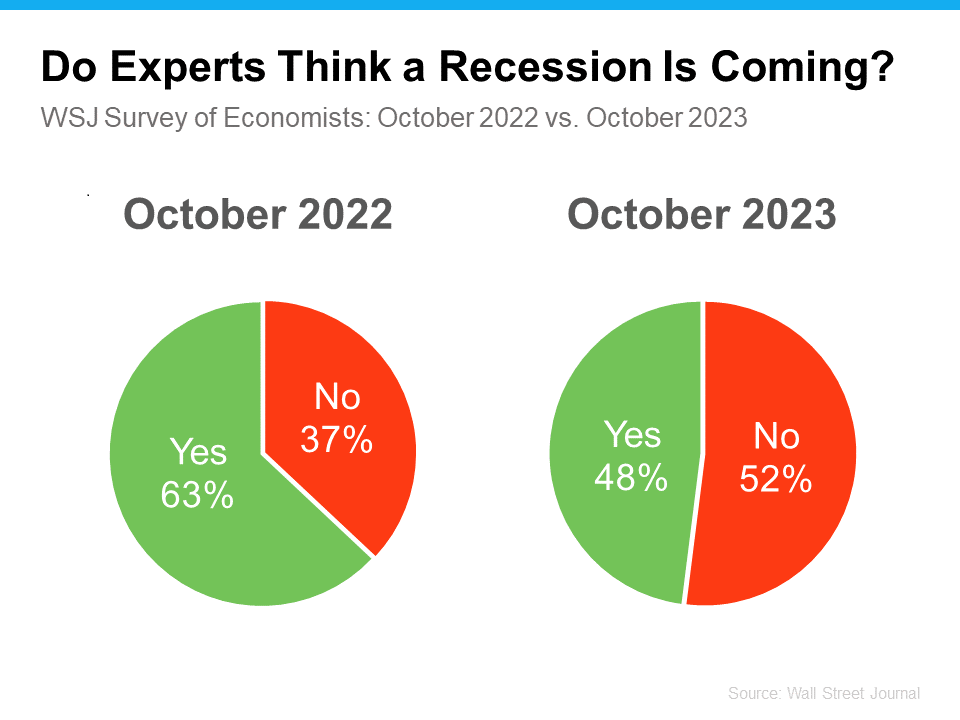

Why the Economy Won’t Tank the Housing Market...

Read more

-

-

Are the Top 3 Housing Market Questions on Your Mind?...

Read more

-

-

How does home staging help increase the value of a home? Read this guide for 5 simple tips on staging your home to attract more buyers....

Read more